Why California Residents Have Stronger Credit Reporting Protections Than Most Americans – And How to Actually Use Them

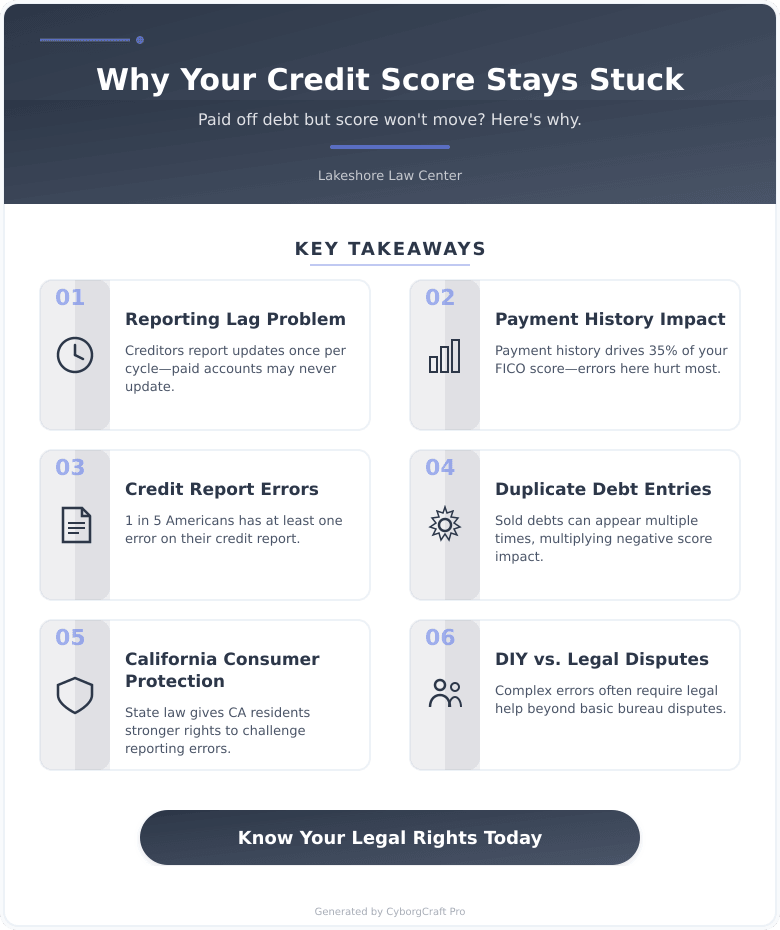

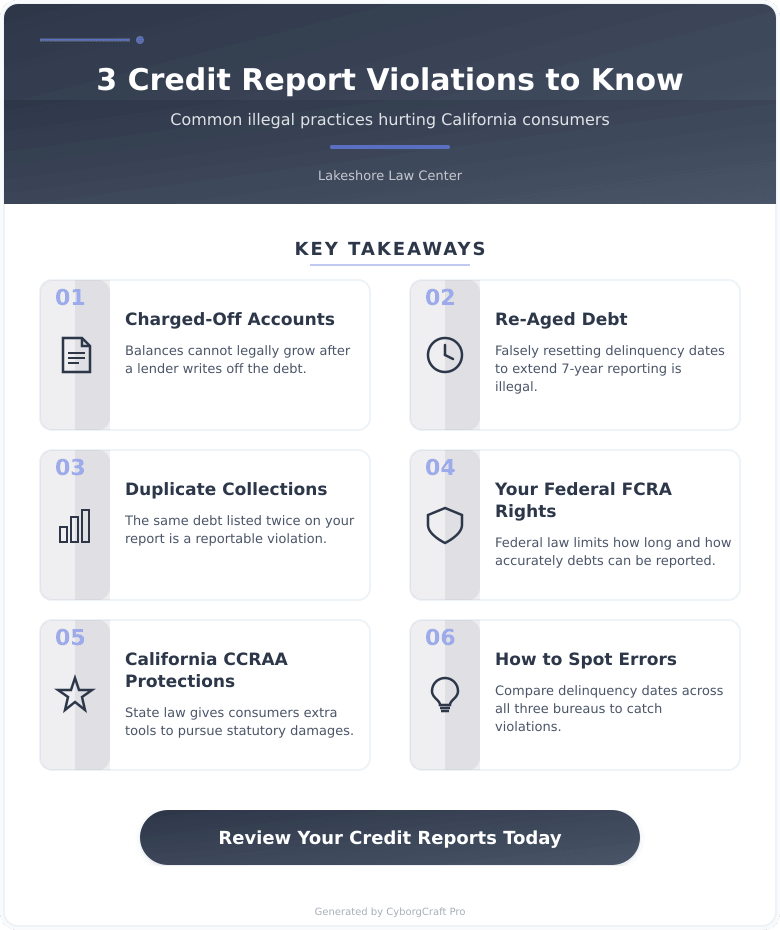

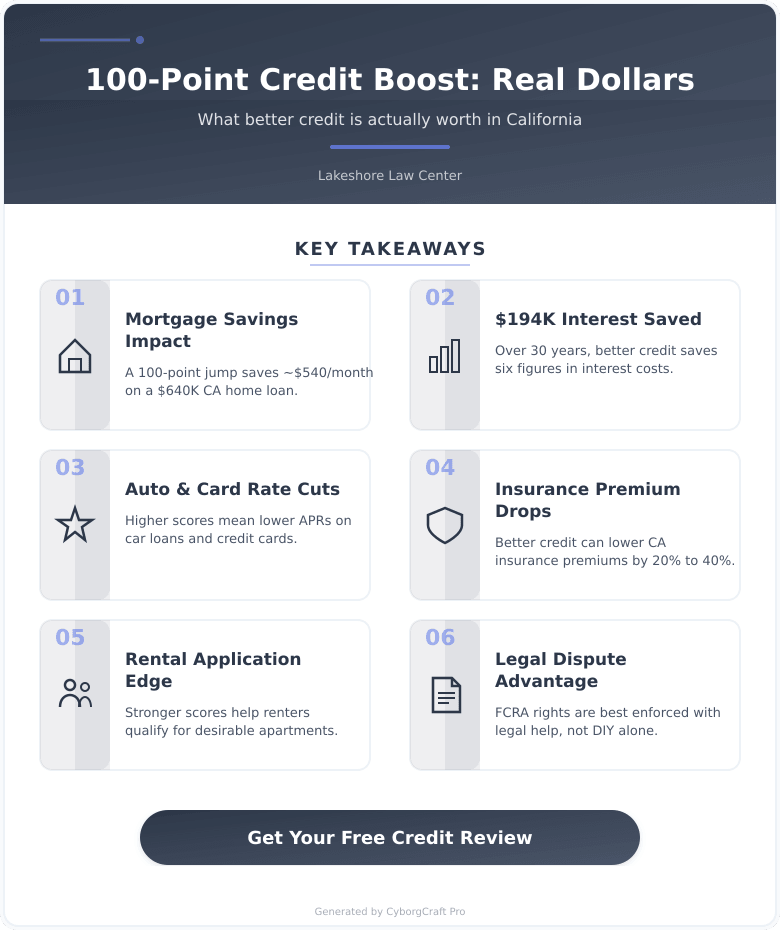

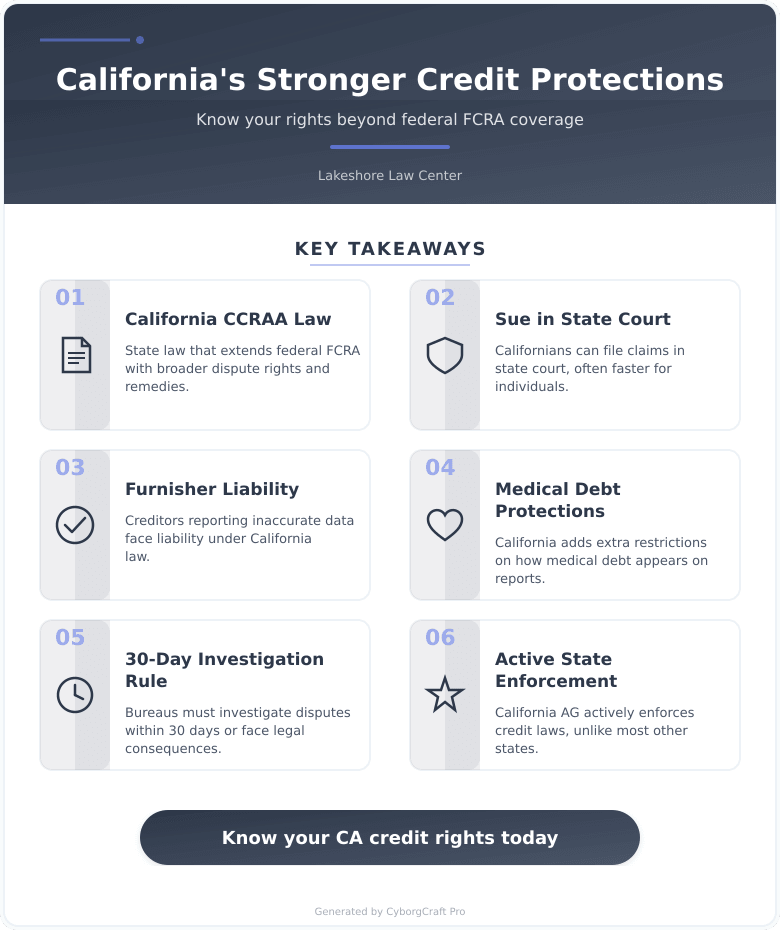

California residents hold credit reporting rights that most Americans simply do not have access to. The California Consumer Credit Reporting Agencies Act extends federal protections by giving consumers the ability to sue data furnishers, pursue claims in state court, and hold credit bureaus accountable for inadequate investigations. This piece breaks down how California law compares to neighboring states like Nevada, Arizona, and Oregon, outlines a practical step-by-step dispute process for 2026, and identifies the most common mistakes that undermine consumer disputes. Medical debt rules tightened significantly in 2025, and knowing how those changes interact with your credit file matters now. Whether dealing with a collection account, an outdated entry, or a creditor who ignored your dispute, California law provides more legal paths than most people realize.